Understanding the Changing Landscape of Federal Student Loan Repayment

The federal student loan system has always been a topic loaded with issues, twists and turns, and plenty of confusing bits. Recently, the U.S. Department of Education has announced significant changes to the federal student loan portfolio—specifically, it will restart interest accrual on loans enrolled in the Saving on a Valuable Education (SAVE) Plan, a program sized up amid legal battles and shifting administrative policies. In this opinion editorial, we take a closer look at the current situation, examine the key factors behind these changes, and offer insights on how borrowers might figure a path through these developments.

A Closer Look at the SAVE Plan

The SAVE Plan was introduced as an alternative to traditional repayment methods, with promises of loan cancellation and zero monthly payments. However, a series of federal court decisions have now declared aspects of the plan unlawful. As a result, the Department of Education is required to adjust its policies and restart interest accrual on impacted loans beginning August 1, 2025. This editorial digs into the developments surrounding the SAVE Plan and the reasons driving these adjustments.

Legal Challenges and Court Injunctions Affecting Government Programs

At the heart of the current policy shift are recent judicial rulings that have blocked the implementation of zero percent interest status for SAVE borrowers. Federal courts ruled that the administration’s attempt to provide nontraditional loan forgiveness measures was out of step with statutory requirements. Simply put, while the Department of Education had regulatory authority under a very narrow provision to prevent borrowers from entering negative amortization, it did not have broad authority to set interest rates at zero across the board.

This situation has led to a significant adjustment, where millions of borrowers who were expecting relief are now faced with the reality of interest beginning to accumulate. With nearly 7.7 million borrowers under the SAVE Plan, the implications of this administrative change have been described as both tense and intimidating.

Impact of Judicial Rulings on Federal Student Loan Programs

Recent court decisions have exposed the tricky parts of administrating large-scale student loan forgiveness programs. Specifically, courts have challenged the promise of loan cancellation paired with zero monthly payments, leading to a growing gap between what was promised to borrowers and what the law permits. With federal courts directing adherence to legal repayment frameworks, the current changes reflect an effort to steer through those judicially imposed restrictions while still attempting to offer a viable path for borrowers.

Interest Accrual and Its Effect on Loan Balances

One of the most critical developments is the decision to resume interest accrual on federal student loans within the SAVE Plan. Beginning August 1, 2025, borrowers will no longer benefit from the previously applied rate that blocked interest accumulation. Instead, interest accrued going forward, though not retroactive, will likely affect the overall cost of borrowing.

How Restarting Interest Accrual Will Affect Borrowers

Many borrowers have been under the impression that the SAVE Plan’s zero percent interest rate would protect them from escalating debts. Restarting interest accrual means that, moving forward, the loan balances for SAVE Plan borrowers will gradually increase—adding a layer of difficulty when planning future financial steps.

This development creates several challenges for borrowers, including:

- Increased overall loan balances that could extend the time required to repay the debt.

- An adjustment period wherein borrowers will need to switch to legal repayment plans to manage their debt responsibly.

- Greater complexity in planning financially, as interest added at a future date may not be easily anticipated in current repayment strategies.

Understanding the Fine Points of Interest Rates and Loan Management

For many borrowers, interest rates are a critical detail when planning loan repayment. Restarting accrual means that the previously expected benefit of zero interest is now off the table. It is essential for those affected to get into a clear understanding of how interest rates work, what it means for the growth of their loan balances over time, and what options remain available for strategic financial planning.

Transitioning to Legal and Sustainable Repayment Options

Given the legal challenges and the need to resume interest accrual, the Department of Education is urging borrowers in the SAVE Plan to switch to other legally compliant repayment options. Among the alternative plans, the Income-Based Repayment (IBR) Plan is being highlighted as a favorable option. The IBR plan, like other income-driven repayment models, adjusts the monthly payment based on a borrower’s income and family size, providing a smoother pathway for meeting repayment obligations.

Exploring Income-Based Repayment Options

The Income-Based Repayment option is designed to adjust monthly payments relative to a borrower’s income, offering a more manageable repayment structure. Key features include:

- Monthly payments that reflect actual income levels, reducing the strain during low-income periods.

- Eligibility for potential loan forgiveness after a specified number of years, provided certain criteria are met.

- A structured approach that aligns repayment with individual financial capabilities.

This option is particularly attractive for borrowers who previously relied on the SAVE Plan’s promises of minimal monthly obligations. However, understanding the subtle parts of income-driven repayment plans is critical. Borrowers should take the time to poke around the small distinctions between various options—like the IBR, Pay As You Earn (PAYE), and Income-Contingent Repayment (ICR) plans—to find the one that best fits their circumstances.

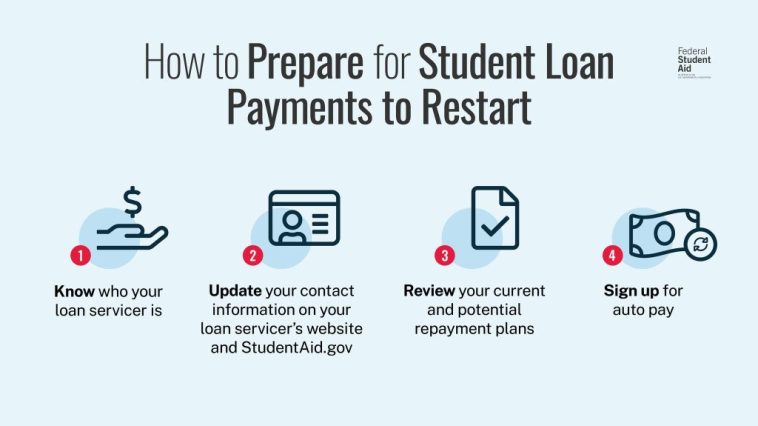

Steps Borrowers Should Take to Switch Repayment Strategies

For those looking to transition out of the SAVE Plan, the Department of Education has set out clear instructions. The process involves:

- Receiving direct outreach from the Department with guidance on selecting a legal repayment plan.

- Using tools like the Loan Simulator, which allows borrowers to estimate monthly payments under various repayment options.

- Reviewing any previous applications for income-driven repayment plans to determine if additional actions are required.

- Ensuring that manner of switching does not disrupt any progress towards qualifying for loan discharge programs, such as Public Service Loan Forgiveness.

Through well-organized outreach and online tools, the transition process is designed to be as smooth as possible. However, despite these efforts, the shift still presents a nerve-racking challenge for borrowers who have grown accustomed to the earlier promises of zero interest and reduced cash flow pressures.

The Broader Implications for Federal Student Loan Policy

This adjustment by the Department of Education is not just a matter of switching repayment plans; it signals a broader rethinking of federal student loan policies. The current situation reveals how administrative decisions, backed by legislative requirements and court rulings, can dramatically affect public policy and public finances.

Policy Shifts and Their Impact on Borrowers and Taxpayers

Recent changes highlight the tension between policy promises and legal realities. For years, proposals labeled as “loan forgiveness” and other relief measures have been popular both politically and electorally. However, when judicial review steps in, the fine points of statutory authority come to the fore. In this case, the administration had to reckon with the fact that despite popular support for sweeping forgiveness measures, the law requires adherence to specific repayment structures.

This dynamic inevitably affects both borrowers and taxpayers. On the one hand, borrowers might feel let down as promised benefits are reversed or altered. On the other hand, taxpayers face concerns about potential financial risks if loan cancellation measures are mismanaged. It is a delicate balance—one that requires policymakers to carefully consider the long-term consequences of any new program.

The Role of Judicial Oversight in Shaping Student Loan Programs

Court rulings have played an essential role in shaping the direction of student loan policy. When federal courts block certain administrative actions, they reinforce the need for legality and fiscal responsibility in how taxpayer money is managed. This instance, involving the SAVE Plan, clearly illustrates how the judicial system acts as a check on executive actions that might otherwise stray from legal mandates.

Judicial oversight not only ensures that federal policies remain within the bounds of the law but also protects the interests of all stakeholders involved. In this scenario, the courts’ interventions have prompted a necessary recalibration that could serve as a model for ensuring transparency and legitimacy in the management of public funds.

Understanding the Hidden Complexities Behind Federal Student Loan Programs

The challenges associated with federal student loans are rarely straightforward. For many borrowers, the transition from programs promising zero interest to legal repayment strategies is a journey through a maze of tangled issues and quiet details. This section examines the hidden complexities behind these programs and the importance of staying well-informed.

Dealing with the Confusing Bits: Interest, Forbearance, and Repayment Assistance

The interest accrual changes present several confusing bits. Supervising the calculation and application of interest in federal loan programs requires an understanding of several key concepts:

- Interest Accrual: Understanding that interest, once it starts accruing, will add to the borrower’s outstanding balance over time if not paid off.

- Forbearance Status: Some borrowers were previously under a forbearance condition that temporarily shielded them from interest, only for this status to be lifted.

- Repayment Assistance: Federal programs like income-driven repayment offer assistance, but they require active management and a willingness to switch plans when legal requirements change.

For many, these fine points are not just bureaucratic details—they are critical for financial planning. Borrowers must dig into these topics to fully appreciate why certain numbers on their monthly statements change and what impact that might have on their long-term financial health.

Understanding the Role of Administrative Wage Garnishment

Another aspect of the new repayment landscape is the potential for administrative wage garnishment. With collections on defaulted federal student loans restarting, mechanisms such as wage garnishment may soon come into play. This possibility should serve as a wake-up call for borrowers currently relying on less intrusive measures.

A few key points about wage garnishment include:

- It is an effort by the government to secure repayment from borrowers who default on their loans.

- The process is designed to automatically deduct payments from paychecks, reducing the borrower’s take-home income.

- It is a measure meant to encourage timely repayments rather than a first step, but it signals that noncompliance will have real financial consequences.

For many, this approach feels like just another intimidating twist in a system already filled with tangled issues. However, understanding these nuances is key to getting around the challenges and planning a way forward.

Taking the Wheel: Strategies for Managing Your Federal Student Loans

Given the evolving policy landscape and the impending resumption of interest accrual, borrowers need to be proactive. Managing your federal student loans in these times means taking responsibility for your financial future, learning about your options, and choosing the path that best fits your unique situation.

Steps to Transition to a Legally Compliant Loan Repayment Plan

With the end of the SAVE Plan’s favorable terms in sight, it is essential for borrowers to adopt strategies that will secure sustainable financial management. Here are some key steps to consider:

- Immediate Outreach: Look for communications from the Department of Education. The agency has indicated that it will begin direct outreach to nearly 7.7 million SAVE Plan borrowers, providing instructions on how to transition smoothly.

- Utilize Online Tools: Take advantage of the Loan Simulator and other online platforms available at StudentAid.gov. These tools can help you compare various repayment plans, estimate monthly payments, and determine eligibility.

- Review Your Current Plan: If you previously submitted an application for an income-driven repayment plan such as the Income-Based Repayment option, review your documentation to ensure that transitioning will not reset your progress.

- Stay Informed: Federal student loan policies can change rapidly. Regularly check official updates from the Department of Education and stay in touch with reputable financial advice sources.

- Consider Future Legislative Changes: Be aware of upcoming programs, such as the Repayment Assistance Plan under the One Big Beautiful Bill Act, which will be available by July 2026, and factor these into your long-term planning.

Taking these steps doesn’t guarantee an immediate resolution, but a proactive approach can help manage the nerve-racking aspects of transitioning repayment strategies. It also empowers borrowers to make informed decisions amidst policies that continuously evolve and present unexpected twists and turns.

Charting a Sustainable Financial Path

Ultimately, the goal for borrowers should be to secure a legally compliant repayment plan that not only minimizes financial strain but also sets the stage for eventual loan discharge or forgiveness under appropriate programs. Key to this process is a mindset of responsibility and adaptability.

Consider the following strategies that might help you chart a sustainable financial path:

- Budgeting and Financial Planning: Adjust your monthly budget to accommodate a payment plan that now includes accruing interest. Even if the changes seem overwhelming, consistent budgeting can help reduce the shock of higher balances.

- Income-Driven Repayment Flexibility: With the availability of income-based plans, explore how your income fluctuations might impact your repayments and plan accordingly. Knowing that your payment can adjust with your financial circumstances can offer some relief.

- Professional Financial Advice: If the new policies seem intimidating, consider consulting with a financial advisor who specializes in federal student loans. They can help you work through the subtle details and points you might not have noticed before.

- Keeping an Eye on Legislative Developments: The dynamic nature of federal student loan policy means that new programs and refinancing options may emerge. Staying informed will help you figure a path through any additional policy changes in the future.

The Role of Transparent Communication in Federal Educational Policy

One of the ongoing difficulties in managing federal student loans is the communication gap between policymakers and borrowers. The recent changes in the SAVE Plan illustrate a scenario where promises made on one hand are counterbalanced by subsequent legal injunctions and administrative modifications.

The Importance of Clear Guidelines and Honest Expectations

For many borrowers, vague promises and shifting policies add layers of confusion to an already tangled situation. Transparent communication is key to ensuring that all stakeholders—students, parents, policymakers, and taxpayers—understand the conditions and expectations governing loan repayments.

More importantly, solid communication helps to reduce the overwhelming nature of these changes by addressing concerns upfront, such as:

- Why interest accrues on certain loans after a period of forbearance.

- What legal requirements led to a shift away from zero percent interest status.

- How incoming repayment plans will better align with both legislative guidelines and borrower capabilities.

Ensuring clarity is a must-have in rebuilding trust between the federal government and borrowers who rely on these programs for their higher education opportunities. With improved outreach efforts and clearer instructions, borrowers can better understand the fine details involved in each repayment option.

Improving Communication Through Technology and Outreach Initiatives

Modern technology offers opportunities to enhance transparency and provide timely updates. The Department of Education’s plan to directly contact nearly 7.7 million SAVE Plan borrowers is a step in the right direction. However, the long-term goal should be to create a continuous feedback loop that addresses borrower concerns in real time.

Some suggestions for improved communication include:

- Interactive Web Portals: Enhance platforms where borrowers can not only access their loan information but also receive real-time updates on policy changes and repayment options.

- Virtual Financial Assistance Workshops: Host online sessions that help borrowers understand complicated pieces of policy changes, demystify the adjustments, and provide practical guidance on switching repayment plans.

- Regular Newsletters: Establish regular email updates that break down recent developments in simple language, highlighting the practical implications for different groups of borrowers.

What This Means for the Future of Student Loan Policies

The current adjustments to the SAVE Plan are a foretaste of potential future changes in federal student loan policies. As legal challenges continue to influence administrative decisions, both policymakers and borrowers have to remain agile and informed. While these changes represent a necessary alignment with legal standards, they also stress the importance of careful planning and transparent communication moving forward.

Anticipating Future Shifts in the Repayment Framework

It is clear that federal student loan policies are in a state of evolution. With programs like SAVE now undergoing major adjustments, the roadmap for loan repayment is rapidly changing. Some key points to watch for include:

- Legislative Developments: New laws such as the One Big Beautiful Bill Act signal future changes in repayment assistance, which could introduce even more repayment options for borrowers.

- Court Rulings: Future judicial decisions could further redefine the boundaries of permissible repayment measures, reinforcing the need for compliance with statutory requirements.

- Technological Advances: Innovations in managing federal student loans will likely continue, including more sophisticated online tools that help borrowers understand and manage their debt.

With these key points in mind, borrowers should be prepared for additional adjustments that seek to align policy with both legal mandates and fiscal responsibility. It is essential to keep a close eye on policy developments and let clear communication guide the transition process.

Balancing Borrower Relief with Fiscal Responsibility

One of the perpetual challenges in federal student loan policy is balancing the need to provide relief for borrowers against the overarching responsibility to manage taxpayer funds prudently. The adjustments to the SAVE Plan underscore this delicate balancing act.

Key considerations include:

- Ensuring Sustainability: Adjustments like restarting interest accrual aim to prevent scenarios such as negative amortization, ensuring that the overall loan portfolio remains fiscally responsible.

- Protecting Taxpayer Interests: Policies must be designed so that benefits promised to borrowers do not inadvertently saddle taxpayers with undue financial burdens.

- Providing Clear Pathways: By offering legally compliant repayment plans, the aim is to secure both borrower relief and long-term sustainability in the federal student loan system.

As the landscape continues to shift, both borrowers and policymakers are tasked with finding an equilibrium that meets immediate needs while laying the groundwork for future stability. The transition away from the SAVE Plan is just one chapter in a much larger story of federal student loan reform.

Final Thoughts: Navigating the Future of Student Loan Repayment

In conclusion, the recent changes announced by the U.S. Department of Education mark a significant turning point for federal student loans. With the SAVE Plan now subject to renewed interest accrual and legal mandates forcing borrowers to move to alternative, legally compliant repayment plans, the task ahead appears daunting for many. However, by taking proactive steps such as leveraging online tools, seeking professional advice, and keeping abreast of legislative shifts, borrowers can steer through the tricky parts and tangled issues of the policy adjustments.

This unfolding scenario underscores the importance of transparent communication, responsible policy making, and continuous engagement with federal updates. It is a reminder that federal student loan policies, while designed to help, are also subject to legal and fiscal realities that can change rapidly. Each borrower’s journey towards repaying their education debt now demands a more hands-on approach, with an understanding that today’s promises may require adjustments tomorrow.

For students, parents, educators, and policymakers alike, the current scenario offers both challenges and opportunities. The situation calls for a thoughtful review of existing policies, an honest discussion about the future of federal student loans, and a commitment to balancing borrower relief with fiscal accountability. As we look ahead, it is essential to appreciate the subtle details of each policy shift and to take a proactive stance in managing one’s financial future.

Key Takeaways for Borrowers and Policymakers

To summarize some of the key points discussed:

| Issue | Implication | Suggested Action |

|---|---|---|

| Restart of Interest Accrual | Loan balances will increase over time once interest is applied. | Transition to legally compliant repayment plans such as Income-Based Repayment. |

| Legal Challenges | Court injunctions are reversing previously promised benefits. | Stay updated on policy developments and review alternative repayment options. |

| Communication Gaps | Borrowers may feel overwhelmed by shifting guidelines. | Utilize official communications, online tools, and professional advice for accurate information. |

| Administrative Changes | Implementation of collections and potential wage garnishment. | Review your repayment strategy and ensure without delay any necessary transitions. |

Both borrowers and policymakers must work together to ensure that the path ahead is clear, legally sound, and financially sustainable. By focusing on transparent communication, staying well-informed, and managing your personal finances strategically, you can face the upcoming interest accrual adjustments with confidence.

Looking Forward With Informed Optimism

The current moment in federal student loan policy is undeniably challenging. Yet it also offers an opportunity to reform and update systems that, over the years, have become riddled with tension. With informed optimism and a proactive stance, borrowers have the potential to adjust to these changes in ways that ultimately benefit their long-term financial health.

As we move further into 2025 and beyond, we can expect additional adjustments and possibly new legislative measures aimed at further refining the student loan repayment framework. It is crucial for all affected parties to take a closer look at each development, understand its impact, and contribute to discussions about how future policies should be structured.

Ultimately, the goal is to create a system where borrowers have clear choices, where financial assistance is aligned with legal requirements, and where the overall balance between supporting individual education and ensuring fiscal responsibility is maintained. While the present changes may seem overwhelming, they also pave the way for a more transparent and robust structure in the future.

Staying Resilient in the Face of Policy Changes

This editorial has aimed to provide a balanced view of the intricacies involved in the recent federal student loan policy adjustments. The twists and turns of the current situation require each borrower to approach their financial challenges with careful thought and preparedness. By staying informed, utilizing available resources, and not shying away from seeking professional help, you can better position yourself to deal with the changes ahead.

In the end, the responsibility for managing student debt is a shared one—one that involves not only individual borrowers but also the policymakers who design these programs. As discussions continue and new policies emerge, it remains essential to advocate for fairness, clarity, and accountability in federal student loan administration. This balanced approach ensures that while borrowers receive necessary support, taxpayer funds are used in a sound and responsible manner.

Conclusion

The evolution of the SAVE Plan and the broader federal student loan repayment framework serves as a reminder of the continual need to adjust public policy in accordance with legal standards and fiscal realities. As interest starts accruing again for SAVE Plan borrowers and new repayment strategies are introduced, the road ahead may appear full of problems and nerve-racking challenges. However, by taking a proactive stance—educating yourselves on the fine points of each plan, leveraging the available online tools, and keeping communication channels open—you can successfully figure a path through these tangled issues.

This piece has aimed to provide a neutral and comprehensive overview of the current developments, along with actionable insights for both borrowers and concerned citizens. It is our hope that by shedding light on the hidden complexities behind these policy shifts, all stakeholders will be better equipped to make informed decisions about the future of student loan repayment and overall educational financing.

In navigating this changing landscape, remember that staying informed, getting into the details of your specific situation, and seeking advice when needed are all super important steps in ensuring that your educational investments continue to be a pathway to opportunity rather than a financial burden. The future of federal student loans may be uncertain, but clear-headed strategies and open dialogue can help everyone involved steer toward a more stable and understandable system.

Originally Post From https://www.ed.gov/about/news/press-release/us-department-of-education-continues-improve-federal-student-loan-repayment-options-addresses-illegal-biden-administration-actions

Read more about this topic at

What is a mortgage reinstatement?

Do I Really Have To Pay Default Rate Interest In Order …